How to Start Again With Money (After You’ve Drifted)

A simple, non-shaming reset to start again with your finances after you’ve... drifted: find your next 3 risks, make 1 move that prevents fees, and set 1 automation to stay on track.

There’s a specific kind of dread that only shows up when you open a money app.

You open your bank app. Your thumb hovers. You see the number and your brain tries to close the app like it’s a hot stove.

Not because you’re reckless. Because it’s easier to live in “I’ll deal with it later” than to feel that spike right now.

I’ve done the close-the-app move more times than I’d like to admit. So this isn’t a “new year, new budget” speech. It’s a start-again plan for normal people (yes, that's you) with messy weeks.

The real problem isn’t drifting. It’s the delay tax.

Drift happens when life eats your attention and money becomes background noise. You deal with the loud thing in front of you, the urgency fades, and the rest gets postponed without a decision ever being made.

Then you start paying the delay tax:

- late fees

- overdrafts

- interest piling up

- shutoff risk

- surprise renewals

- background dread that makes you avoid it even more

Late fees and overdrafts aren’t “consequences.” They’re a tax on being busy. Starting again is how you stop paying it.

If you only do one thing, do this

If you do nothing else, do these three things:

- Find your next 3 risks (with dates).

- Do 1 move that prevents the most damage.

- Set 1 automation so this doesn’t rely on willpower.

That’s a restart. Everything else is optional.

How to get back on track financially: the Start-Again Reset (25 minutes)

Give yourself 25 minutes. This is not “fix my finances.” This is stabilize the next 7–10 days.

Minute 0–6: Open everything (no self-roasting)

Open:

- checking

- credit cards

- any “pay-in-4” thing you’re using, aka paying in installments

- the account where your biggest bills hit

No interpreting what it “means.” Just open it and look.

Minute 6–12: Find the next three risks (dates included)

Write down the next three things that could hurt you in the next 7–10 days if you ignore them.

Examples:

- a bill that will bounce

- a card about to go past due

- an autopay that will overdraft you

- a shutoff notice

- a subscription renewal you forgot existed

Keep it to three. Three keeps you out of the “everything is on fire” spiral.

Minute 12–22: Make one move that prevents the most damage

Pick one action that reduces future consequences today.

Decision rule:

Choose the move that prevents the most fees, shutoffs, or – eek! – a chain reaction of them all.

Good “one moves”:

- Pay the minimum on the card that’s about to go past due.

- Pay the bill that causes the biggest chain reaction if it fails (rent, car insurance, power).

- Move money so a scheduled autopay won’t overdraft you.

- Cancel the subscription that hits in the next 48 hours.

- Ask for a one-time fee waiver (script below).

If you’re stuck: pick the earliest due date or the nastiest penalty. Dates and penalties don’t care about good intentions.

Minute 22–25: Set one automation (so you don’t have to be “good” forever)

One automation. Not a life overhaul.

Pick one:

- Autopay minimums on credit cards (boring, effective, stops the late-fee spiral).

- Automatic transfer: $25–$100/week into a buffer account.

- Calendar reminders for the top 3 bills you repeatedly miss.

- Low-balance alerts (set them higher than you think you need).

Motivation comes and goes. A calendar reminder doesn’t.

The Start-Again Page (copy/paste into Notes)

This is the whole thing. Use it anytime you drift.

Cash on hand: $_______

Money coming in (next 7 days): $_______

Next three risks (with dates):

- ______ due ______ (penalty: ______)

- ______ due ______ (penalty: ______)

- ______ due ______ (penalty: ______)

One move I’m doing today (prevents most damage):

One automation I’m setting today: _____________

Tomorrow’s 10-minute follow-up:

- Cancel / reduce / renegotiate: __________________

Want this as a one-page printable + the scripts below? Comment START and I’ll email you the one-page version.

A real-world example

Here’s a pretty typical week when you’re short and avoiding it.

Checking: $412

Paycheck expected Friday: $740

Upcoming hits:

- Phone autopay: $96 Tuesday (overdraft risk)

- Car insurance: $189 Wednesday (lapse risk)

- Credit card: $215 Thursday (late fee + credit hit)

- Plus a $14.99 subscription renewal you forgot about that hits whenever it feels like it

Next three risks:

- Phone autopay Tuesday — overdraft

- Car insurance Wednesday — lapse

- Credit card Thursday — late fee / credit hit

One move today: stop the overdraft and protect the insurance.

- If your phone provider lets you: move the autopay date to Friday so it lines up with the paycheck.

- If not: turn off autopay and plan to pay it manually Friday so it can’t hit at the worst time.

- Then make sure the car insurance gets paid. A lapse is expensive in ways that don’t show up on a budget sheet.

One automation: autopay minimums on the credit card.

Not because it’s ideal. Because it prevents the “late fee → more avoidance → more late fees” loop.

Tomorrow’s 10 minutes: message insurance and ask to align due dates to payday.

Notice what didn’t happen:

- no budget rebuild

- no new app

- no tracking every transaction

Just stability.

Restarting your budget after falling off (without making it a whole project)

When people say “I fell off my budget,” they usually mean:

- I lost visibility, and

- it became emotionally expensive to look.

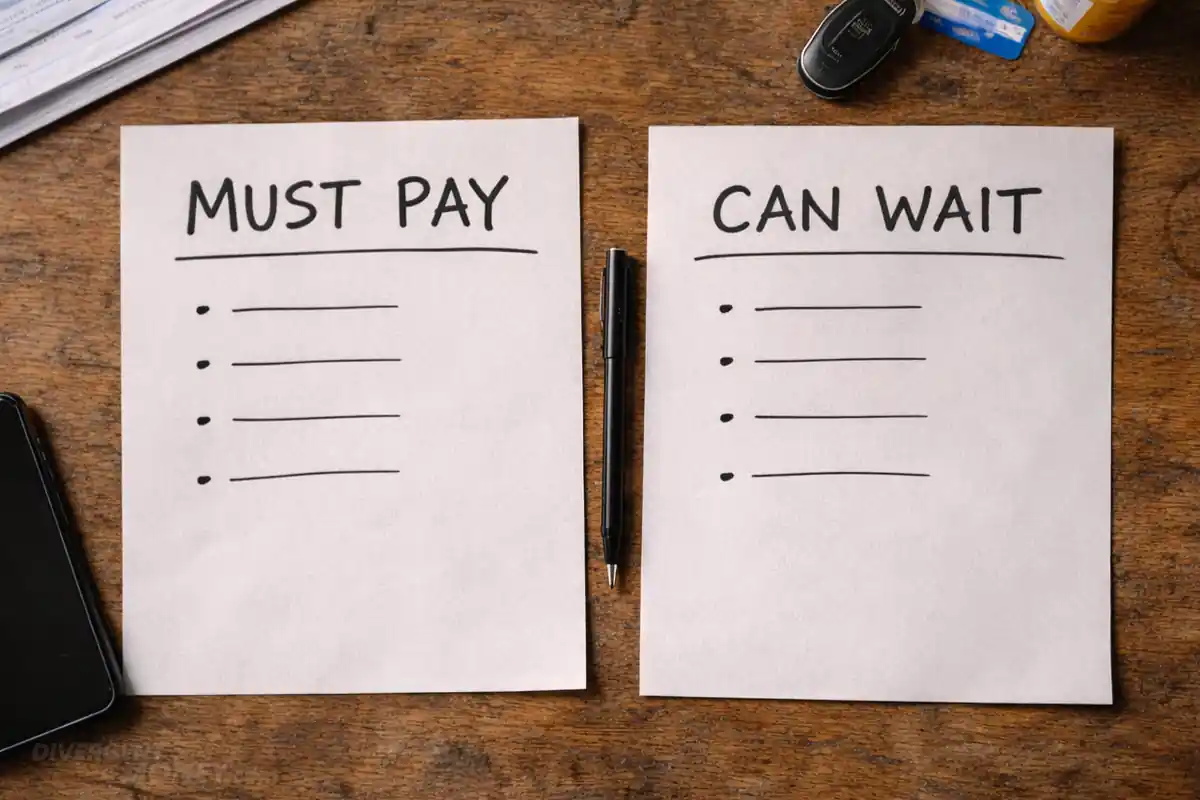

So don’t restart with a full rebuild. Restart with a floor.

Step 1: Two lists

MUST PAY (keeps life running):

- housing

- heat/power

- transportation (if it keeps you functional)

- minimum debt payments (to avoid penalties)

- meds/childcare/true essentials

CAN DELAY (with a call or click):

- medical bills

- subscriptions

- non-urgent services

- anything with a grace period or payment plan

If you’re short, you’re not “being bad at money.” You’re doing triage. The goal is prevent the most expensive outcomes.

Step 2: Find the number you’re living with this week

Calculate:

- money coming in this week (real deposits you expect)

- minus must-pay items due this week

What’s left is the number you’re living with this week.

That number isn’t a verdict. It’s just what you’re working with this week. Once you have it, dread turns into decisions.

Two scripts that save real money (and stress)

Script 1: One-time fee waiver (call or chat)

“Hi — I’m seeing a [late fee/overdraft fee] from [date]. I’m bringing the account current today. Can you waive this as a one-time courtesy?”

If they say no:

“Can you transfer me to someone who can review a courtesy waiver? I’d appreciate it.”

Short. Calm. No life story required.

Script 2: Buy time on a bill you can’t pay yet

“My payment is due on [date]. I can’t make the full amount by then. What options do you have for an extension or payment plan so I can avoid penalties?”

Then let them talk. Your job is terms, not confession.

Two quick “stop paying the delay tax” moves

If you want a couple fast wins that don’t require a personality transplant:

- Stop overdraft roulette. Turn on alerts. Move autopays to payday. Turn off autopays that hit unpredictably.

- Stop letting minimum payments depend on memory. Autopay minimums is boring — and that’s why it works.

Yes, you can optimize later. Right now you’re buying breathing room.

The line to keep

Starting again isn’t renovating the house. It’s turning the lights on.

Look at it. Fix one thing that would bite you. Put one safeguard in place. Then stop.

Quick question (so the next post hits)

When you drift, where do you get stuck?

- opening the accounts

- seeing the numbers

- choosing what to do first

- staying consistent after day one